NAVIGATING CYCLES

Introduction

Two years ago, we outlined our belief that the world of tomorrow can be substantially better than the world of today. This was despite the backdrop of soaring inflation, falling financial markets and a tumultuous UK government.

Indeed, progress rarely happens in a straight line. It requires enduring a litany of short-term challenges. This is why we pay close attention to the many cycles at work in the investment world: of demand and supply, of expectations and valuation, and even of the price of money as expressed in borrowing rates.

Understanding these dynamics allows us to improve portfolio returns and manage risk. It helps us to tilt toward areas of opportunity when investing in companies and ensure portfolio resilience to withstand the unavoidable setbacks.

DEMAND CYCLES: COVID-INDUCED HANGOVERS

The shadow of Covid continues to fall long. The pandemic caused many companies, previously used to steadily rising orders, to be suddenly swamped by booming demand. However, the end of Covid brought a slowdown equally as extreme.

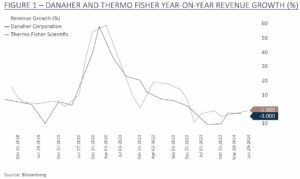

Such rapid adjustment is throwing up opportunities for investors like us, willing to look through that cycle. This is exemplified by life sciences businesses Thermo Fisher and Danaher.

These companies provide a royalty on medical innovation, selling analytical instruments and tools to pharmaceutical firms, academia and industry. For years, breakthroughs have been accelerating as advances in fields such as cell and gene therapy combine with faster regulatory approvals for treatments targeting previously unmet needs.

Ordinarily these companies generate over three-quarters of their revenues from recurring sources. Their products are required every day and their sale follows the global growth in research and production. Most of the time, these annuity streams sit in the background, far from the political spotlight and immunised to peaks and troughs in demand.

However, during Covid these companies were thrust to the foreground, providing the picks and shovels in the race to develop vaccines and diagnose patients. As innovation accelerated, demand spiked and growth was turbo-charged. Thermo Fisher and Danaher’s revenues both grew around 60% in just two years.

However, as Covid transitioned from pandemic to endemic, those tailwinds faded. This was exacerbated by many customers finding they had over-stocked; the laboratory equivalent of buying mountains of toilet roll and pasta. Combined, this drove year-on-year growth into negative territory.

Yet there has been no change to the beneficial secular trends and these companies’ ability to grow significantly in the decade to come. Furthermore, both Thermo Fisher and Danaher used the additional cashflow from Covid sales to enhance their businesses, expanding capacity and acquiring new capabilities.

Looking through the unsettling gyrations in demand provides us an opportunity to buy stronger companies at lower prices. Our ownership in Thermo Fisher and understanding of the cycle prompted us to add Danaher to our roster.

Supply Cycles: Unpicking Capital Investment Plans

Over many years, capital allocation is the key ingredient in the recipe for outstanding equity returns. As Warren Buffett noted back in 1987: “After ten years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.”

This is particularly true given our approach. We invest in companies that generate higher returns on capital than the average publicly-quoted company and retain a greater proportion of their earnings to reinvest for future growth.

We then usually hold our companies for much longer than others. The average company has been on our ‘Buy List’ for many years and we have invested in some for over a decade. By contrast, US stocks are now commonly held for less than a year.

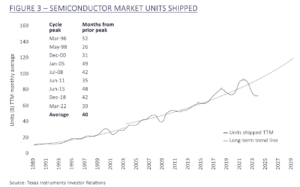

Greater retention of earnings over longer stretches of time means selecting managers who skillfully allocate capital is paramount. We spend considerable effort unpicking corporate investment plans, such as those of Texas Instruments.

Of all the technology world, semiconductor production has been the most prone to boom and busts. Capital tends to flood in during good times, funding new production facilities and driving down returns, just in time for demand to wane and capital to flow back out.

Historically, Texas Instruments has side-stepped this in its niche as the leading manufacturer of analogue semiconductors. These are the building blocks for electronic systems, managing the flow of electricity or converting real-world signals such as sound or pressure into digital signals that a computer can process. They can be found in devices from the crash bag in your car to the solar panel on your roof.

Accordingly, it intrigued us when Texas decided to invest nearly $30bn to expand its production sites counter to the cycle.

In the last two upswings, demand for semiconductors to electrify vehicles and automate industry grew over 10% a year. At the height, Texas had to turn away orders. We are now over 3 years into a downtrend that has driven shipments back below 2019 levels.

In an industry where size matters, Texas is already twice as large as its closest peer, Analog Devices. Expanding scale supports product breadth, sale capabilities and makes it economically viable to manufacture more in-house and on newer technology. This increases its cost advantage versus rivals and puts the right capacity in the right location amidst rising geopolitical anxieties.

These features showcase what we like. A long-standing management team investing against the grain to increase their competitive advantages at a time when demand is cyclically depressed. The cherry on the cake is that US government tax incentives are paying for much of the investment. This should support double-digits growth in free cashfiow per share. Shareholder returns should follow.

VALUATION CYCLES: THE PRESSURE OF GREAT EXPECTATIONS

One of the challenges in owning quality companies is when hopes get too high, they can become expensive.

Fair value is an abstract concept. For many it makes little sense to even bother trying to assess the real value of a business given their short time frames. It is simply easier to forecast the future by extrapolating the past, combining liberal helpings of ‘recency’ and ‘anchoring’ bias with the tendency to make linear forecasts despite economic life being cyclical.

This finds outlet through the valve of valuations – how much someone is willing to pay to buy or sell an investment- creating the momentum that makes dear shares become more expensive and cheap shares become cheaper.

If you invest in companies earning high returns on capital, this makes little difference over the long run. But over short periods of time a fall from grace can be costly. Imagine you buy a company hoping it will grow its earnings by 10% a year for three years and decide to pay 33x forward price/earnings. The company grows as expected but its valuation derates by 25% to 25x. Your return evaporates.

A current conundrum is Amphenol.

The company makes electronic connectors, antennae and sensors for everything from mobile telephone networks to cars, an enabler of the electrification of the world. Since we became shareholders in 2015, the company has performed strongly. Its earnings have compounded at 16% and its shares returned 18% annually, handsomely outperforming global stock markets.

However, as the gap between the earnings and returns highlights, the company has become expensive. It trades near its highest all-time valuation with analysts expecting faster growth than in the past.

This refiects how enthusiasm has swelled that Amphenol’s high speed, low latency interconnectors will power artificial intelligence (Al) datacentres. A new Nvidia rack of 72 graphics processing units needs 5,184 such cables and these racks are fiying off the shelves into the arms of customers who can’t afford inferior parts.

So, what to do?

One option is to trim positions in the hope of repurchasing the same shares when they are lower. This can make sense when valuations are egregious. However, timing markets is notoriously hard.

A preferable solution is to use today’s expensive investments to identify fresh opportunities.

Amphenol’s culture of adaptability is impressive. Its decentralised operations empower frontline employees to act entrepreneurially at the coalface of customer interactions. This helps the business change course with technology and demand while allowing Amphenol to add complementary businesses through acquisition.

This led us to AMETEK.

In terms of what it does, AMETEK bears scant similarity. The company manufactures highly-engineered products ranging from precision motion control solutions for factory automation to test and measurement instruments in commercial aircraft.

Rather, it is in how AMETEK does business that the resemblance lies. It too is built on a decentralised approach, using 40 operating units to sell tens of thousands of products to diverse customers spanning the healthcare to industrial arenas. Each unit has the autonomy to make decisions as they see best with excess cash sent back to headquarters to fund purchases of privately-owned businesses.

Over 20 years, AMETEK has delivered 17% annualised returns for shareholders. Yet AMETEK trades at the low end of its valuation range relative to its own history and the wider global stock market; an appealing prospect given the quality of the business and growth outlook. It has been overlooked of late by investors searching for anything Al.

Such pattern recognition helps us navigate the waves of optimism and pessimism that affect companies and their share prices. It’s why we benefit from being generalists. Analysts who examine opportunities across the market are less prone to entanglement in the thickets of specific industries and single cycles.

To avoid missing the wood for the trees, we like to ask company management teams: ‘if you couldn’t own shares in your own business, whose shares would you own?’ Not only does this uncover a leader’s intellectual curiosity (or lack of), it can prove gold dust when they complement a peer. When asked in our offices, Amphenol’s CEO Adam Norwitt answered ‘Texas Instruments’.

INTEREST RATE CYCLES: BONDS ARE BACK

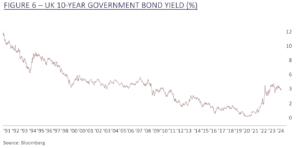

Perhaps the greatest shift of recent years has been in the bond market. Usually one of the calmer tidal estuaries, its extreme ebbs and flows have materially impacted the sources of protection for client portfolios.

At JH&P we view bonds as a line of defence for those clients who need it when equity markets inevitably stumble.

While bonds offer more modest returns than owning company shares, they represent a hedge against financial accidents which tend to happen when they are least expected. They are a trade-off between the uncertainty of today and the promise of tomorrow.

Accordingly, our bond holdings have largely been those issued by UK and US governments. These bonds are highly secure backed by the ability of governments to tax their populations. Except in moments of turmoil (viz. Liz Truss ‘moment’), their safety is rarely questioned.

Unfortunately, these promises became inordinately expensive as the experiment of zero interest rates and quantitative easing collided with the Covid pandemic.

Since 1990 an investor would on average have received a return of 4.6% per year for lending to the UK government for a decade. By April 2020, the prospective 10-year return had fallen to 0.08%. For the safety of getting your money back, an investor would receive no return even before the erosion of inflation. Even the safest investment can be made risky by too high a price.

Faced with such unpalatable fare, we moved significantly underweight bonds and shortened our duration, financial parlance for ensuring we were less exposed to bonds becoming cheaper.

We then sought new forms of armour. We turned to diversifying funds that could offer returns that were insulated from bond or equity movements. And we turned to gold. Gold is a funny asset because it produces no cashflows. Like an Old Master painting, its value lies in the eye of the beholder. Yet, time and again, gold has proven valuable when the nuclear sewage hits the windmill.

These actions helped us when inflation surged amidst the Ukraine war and the after-effects of Covid. Bonds experienced their worst decline in a generation. By contrast, our diversifying funds and gold proved resilient. Financial fortunes rest not just on capturing gains but on avoiding losses. These steps were the best example of the latter since our firm started in 2010.

The silver lining of poor bond returns in the rearview mirror is more attractive returns looking through the windshield. UK and US sovereign bonds once again offer a reasonable rate of return. We have rebuilt our positions where appropriate while our diversifying funds and gold have continued to prove valuable.

HOUSING CYCLES – WHERE NEXT?

Financial markets offer few single-edged swords. While the rise in interest rates has helped lenders, it has punished borrowers especially those seeking new mortgages. We know this will provide opportunities.

The US economy remains the largest in the world, making up a quarter of global activity, and its beating heart is the consumer whose spending drives over two-thirds of the nation’s gross domestic product.

While an Englishman’s home is reputedly (and occasionally literally) his castle, the American Dream rests on home ownership. Owning the place where you bring up your family is a badge of success, providing psychic income as well as financial rewards. These attractions are not lost on US individuals. Gallup asks Americans what they think the best long-term investment is and every year since 2013, real estate has topped the list.

However, a house is usually the biggest single household purchase, and most can’t achieve this without borrowing. For many years borrowing was affordable with US house prices reasonable relative to income and mortgage rates low.

This changed in 2022 with the average US 30- year mortgage rate rising from 3% to 8% at the high in October 2023, double the average rate since 1990. Coupled with house prices c.50% above their pre-Covid levels, this has put the property ladder out of reach for many.

Making things worse, unlike in the UK, US mortgages don’t move with their owners. There is little incentive for existing homeowners to relocate and swap a 3% mortgage for a 7% one.

The result? A gummed-up market. Housing turnover is at its lowest level since the Global Financial Crisis and housing inventory is near its nadir.

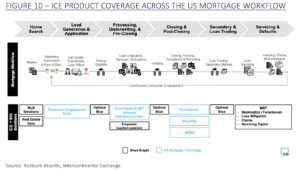

Falling interest rates offer hints of hope and opportunities are appearing, such as Intercontinental Exchange (ICE).

Founded in the 1990s by the current CEO, ICE is a global provider of data and technology, owning the New York Stock Exchange and dominating energy markets. However, ICE’s fastest-growing and most profitable division is its mortgage technology business.

The cost of purchasing a US home is high and rising. Buying a $1m home with a 20% deposit could involve nearly $20,000 of closing costs of which only a fraction can be rolled into the mortgage. Meanwhile, it takes on average 60 days to close a purchase loan due to the cumbersome process. Slow and inefficient, the US mortgage market is also vast, with $390bn of volumes in Q2 2024 despite depressed conditions.

This presents a ripe opportunity for modernisation and ICE is best placed to deliver. Its tools can speed mortgage applications along with fewer human touches and less cost. Helped by an appealing valuation, we are excited by this setup.

We think more openings will appear if the US housing market starts to unlock.

CONCLUSION

There are few certainties in investing. One is the inevitability of cycles, built upon the back of the age-old human tendency to swing from one extreme to another.

Today, we find ourselves facing a laundry list of cyclical challenges, from the growing risk of a US recession as unemployment ticks up to the impact of military conflict after a period of relative quiet. Yet, many of our companies appear well positioned in the context of their own demand and supply phases and we have portfolio protection available to us that was unobtainable for much of the recent past.

Remaining attuned to these cycles allows us to identify the clouds gathering on the horizon in one direction while spotting where they might be starting to disperse in another. We are hopeful that this should underpin higher returns in the years to come and provide a vantage point from which to allow a new wave of investors to learn an old set of lessons.

Article written by Thomas Allsup, Porfolio Manager

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SWl Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.