Patrick Trueman, Portfolio Manager

The long-term investment case for owning integrated oil companies – those that operate across the entire petroleum value chain from rig to pump – is fraught with challenges.

In the wake of the pandemic, global oil demand is expected to fall this year by a record 9.3 million barrels a day. That is the equivalent of India’s total annual consumption1.

China has just pledged to be carbon neutral by 2060. Other countries around the world are targeting carbon neutrality by 2050 – including, most recently, Japan and Korea. The US remains an outsider – but a different incumbent in the Oval Office could change that. Joe Biden has pledged to invest $1.7 trillion in making the US a 100% clean energy, net-zero-emissions economy by 2050.

As governments introduce regulations to start driving the necessary change, individual companies are quickly declaring their own targets.

This should lead to lower fossil fuel consumption, you might think. But forecasts for oil demand vary vastly.

Drilling down

Many believe that demand will actually carry on rising through the next 20 years, driven by growing demand in developing countries, if the world returns to its pre-Covid path.

The International Energy Agency (IEA) says that even if governments take the necessary radical measures to achieve their ambitious 2050 net-zero goals it will still be a few years before we see peak oil demand globally. It will take time for new technologies and energy-saving initiatives to kick in. The IEA forecasts that demand will then fall by more than 50% in advanced economies by 2040 and by 10% in developing economies2.

The International Energy Agency (IEA) says that even if governments take the necessary radical measures to achieve their ambitious 2050 net-zero goals it will still be a few years before we see peak oil demand globally. It will take time for new technologies and energy-saving initiatives to kick in. The IEA forecasts that demand will then fall by more than 50% in advanced economies by 2040 and by 10% in developing economies2.

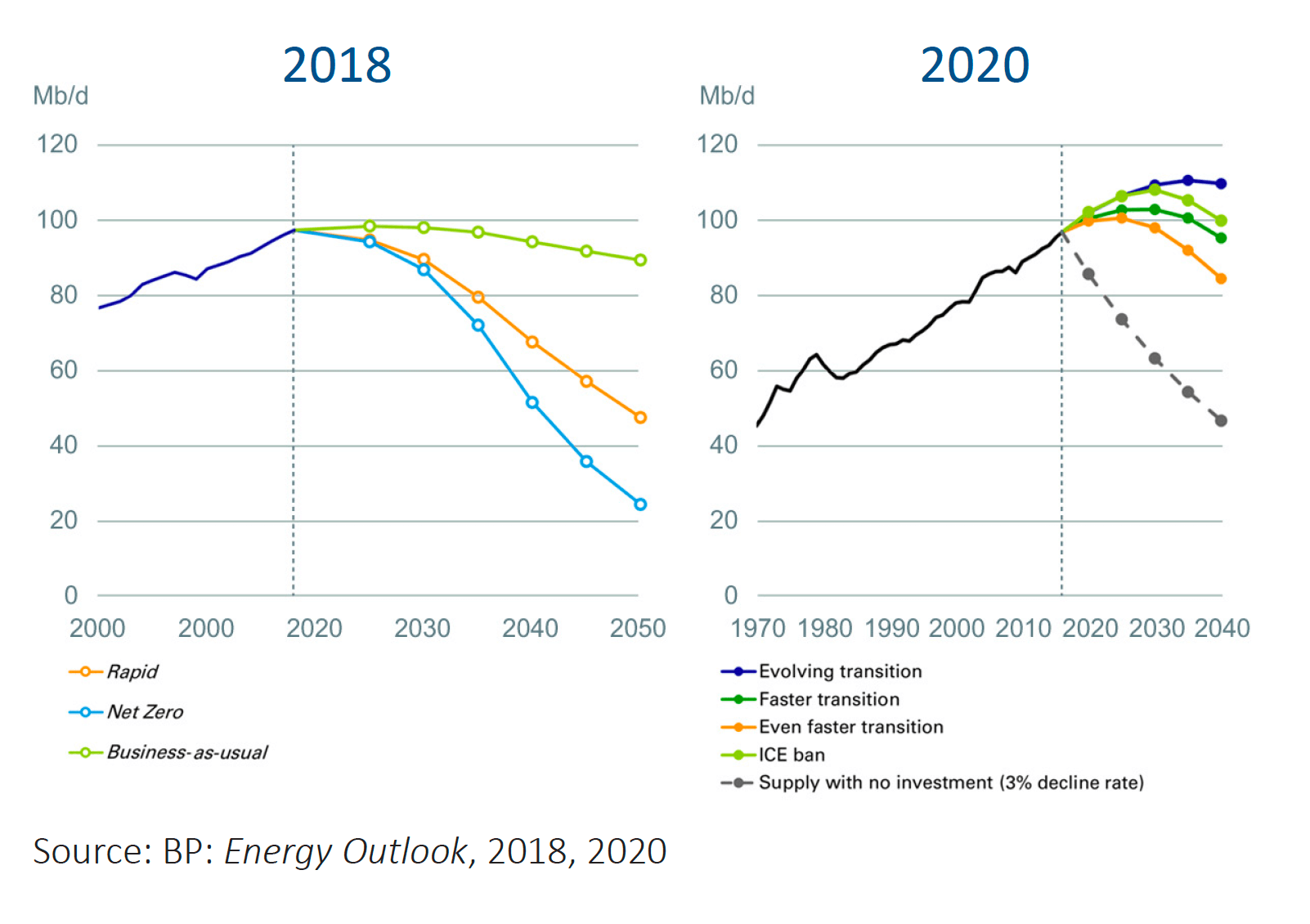

But it is interesting to see how BP’s own forecasts have changed in just a couple of years. In its 2018 outlook its forecasts for fossil fuels concluded that demand would rise for a few more years3. Interviewed by the FT in May this year, BP’s new CEO, Bernard Looney, was asked: “Could it be peak oil?” His conclusion: “Possibly, possibly. I would not write that off.”4

In its most recent official forecasts, published in September, BP mapped out three main scenarios. “Rapid” is based on a series of aggressive policy measures, led by a significant increase in carbon prices. “Net zero” assumes that big shifts in societal behaviour reinforce the policies. “Business as usual” assumes that regulations, technology and social preferences evolve at the rate witnessed in the recent past. In the first two scenarios we are past peak oil. In the third we are very close to it5.

Tides of change

Historically, “peak oil” meant when supply would peak. Our concerns were that we would run out of oil. Today the debate has shifted to demand.

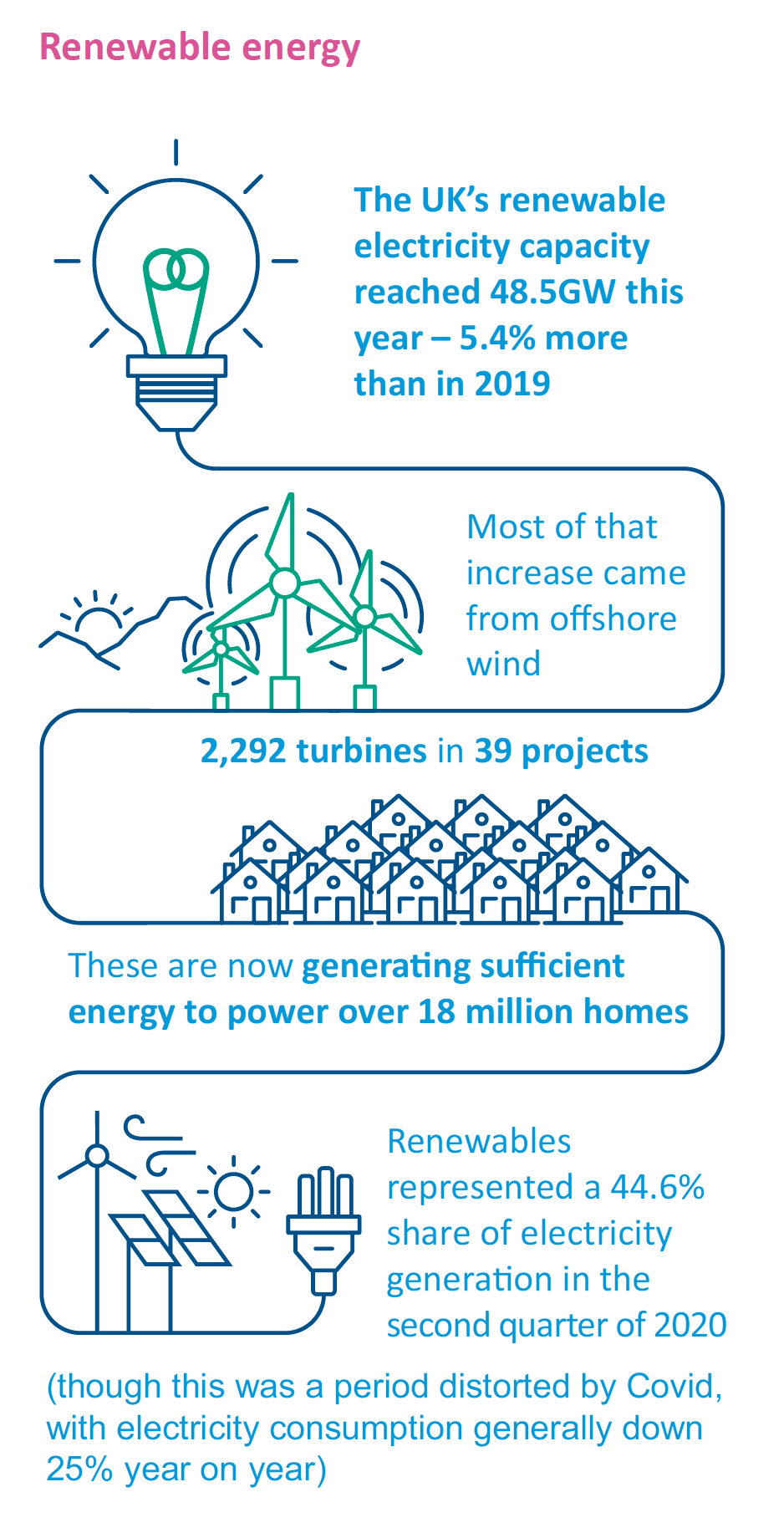

A growing proportion of the global demand for energy is now being satisfied by renewable energy. The UK’s renewable electricity capacity exceeded the total from fossil fuels in the second quarter of this year6, rising to a 44.6% share of electricity generation (though this was a period distorted by Covid, with electricity consumption generally down 12%). Overall, low-carbon electricity (including nuclear) accounted for 62.1% of electricity generated. Coal generation fell to record low levels – there was a 67-day coal-free period in Great Britain between March and June, the longest since the 19th century.

Almost half the demand for oil in the OECD comes from road transport7. It will be some time before electric and hydrogen vehicles replace this, but as the transition happens the demand for electricity is likely to rise and renewables will play a vital role in satisfying that demand if we are to move away from coal generation.

Most of the increase in renewables came from offshore wind – 2,292 turbines in 39 projects are now generating sufficient energy to power over 18 million homes8. And more are planned. Solar generation is also at record levels.

Spencer Dale, BP’s Chief Economist, says that wind and solar power, bioenergy and geothermal energy could account for as much as 60% of primary energy by 2050. He says: “Renewables are penetrating the energy system more quickly than any fuel ever seen in history.”9

Peak oil

Few doubt, therefore, that oil will be left untapped. And shrinking demand usually means shrinking prices.

Figure 1:

How BP’s forecasts for oil demand have changed in two years

Sinking oil prices

This year the price of Brent crude has dropped to around $40 a barrel. At that rate it is unprofitable to extract half the planet’s remaining oil reserves. Most of the oil majors are bracing themselves for permanently low prices. Shell, which in its most recent annual report assumed $60 a barrel, now forecasts $40 in 2021 and $50 in 202210. BP is working on an average of $55 from next year until 2050 (down from $70)11.

With tight oil (extracted from oil shale) offering an abundant source of supply that is relatively easy to extract, companies are jettisoning unprofitable oil fields around the world. In July BP and Shell announced write-downs of up to $17.5bn12 and $22bn13 respectively on assets.

Some analysts believe this may result in a short-term squeeze on demand. Research company Bernstein warns: “Small imbalances between supply and demand of a few percent can result in large price swings in Brent.” It argues that an effective Covid vaccine would be an obvious catalyst. That may be the case, but this feels like a swan song for the commodity.

Impact on share prices

In the past year BP and Shell have both seen their share prices fall by over 60%14. Meanwhile, clean power stocks have risen 45%, according to the Economist15.

In the past year BP and Shell have both seen their share prices fall by over 60%14. Meanwhile, clean power stocks have risen 45%, according to the Economist15.

For decades the oil majors have been stalwarts within many investor portfolios because of their ability to generate cash, distributed in the form of generous dividends. In April Shell cut its dividend for the first time since the Second World War – slashing it by two thirds. In August BP halved its dividend on the back of heavy losses and announced 10,000 job cuts. That same month, in the US, Exxon Mobil – once the world’s largest company – was ejected from the Dow Jones Industrial Average, an index of 30 of America’s biggest companies.

A glimmer of hope?

It seems clear that the integrated oil companies have to change if they are to survive in a world battling to limit global warming to 1.5°C.

In the noughties BP appeared to be ready for that transition, with its “Beyond Petroleum” rebrand. It soon retrenched to oil and gas again. Now it is more committed. In February Looney announced the company’s ambition to be net zero by 2050. This would mean a reduction of around 415 million tonnes of emissions – not far off the total annual emissions of the whole of the UK16. In August more details were given17. BP expects to deploy 20% of its capital in transition businesses, including low-carbon companies, by 2025 and to cut oil and gas production by 40% within a decade.

“Small imbalances between supply and demand of a few percent can result in large price swings in Brent.”

The company intends to invest $5bn a year into low-carbon electricity and energy projects by 2030 – it made its first move into offshore wind in September18. It expects to increase its renewable generation capacity 20-fold, from 2.5GW last year to 50GW, by 2030. Most of this will be in wind and solar, but it is also exploring bioenergy, carbon-capture utility and storage and hydrogen.

France’s Total expects to generate around half its power from renewables by 205019. Shell and Italy’s Eni have also pledged to redirect investments towards renewables.

One advantage for the oil majors is that they have the existing infrastructure for selling power. BP has 3,000 energy traders globally, and Shell manages power trading in over 20 countries20. The European integrated oil companies have a key part to play in the transition to electric vehicles. They have around 90,000 retail stations and are investing in charging points – Total alone is targeting 150,000 in Europe by just 2025.

They are also already established investors in renewables. Shell’s ethanol business (produced from sugarcane in Brazil and corn in the US) has been estimated to be worth $2bn and BP’s $1bn. This new wave of investing could make a significant contribution to the renewables sector that many of the plans for a net-zero world rely upon.

But it will take some time for renewables to generate a meaningful contribution to profits. An onshore windfarm, for example, has a two-to-three-year lead time between investment decision and first power generation, while offshore farms can take 10 to 15 years.

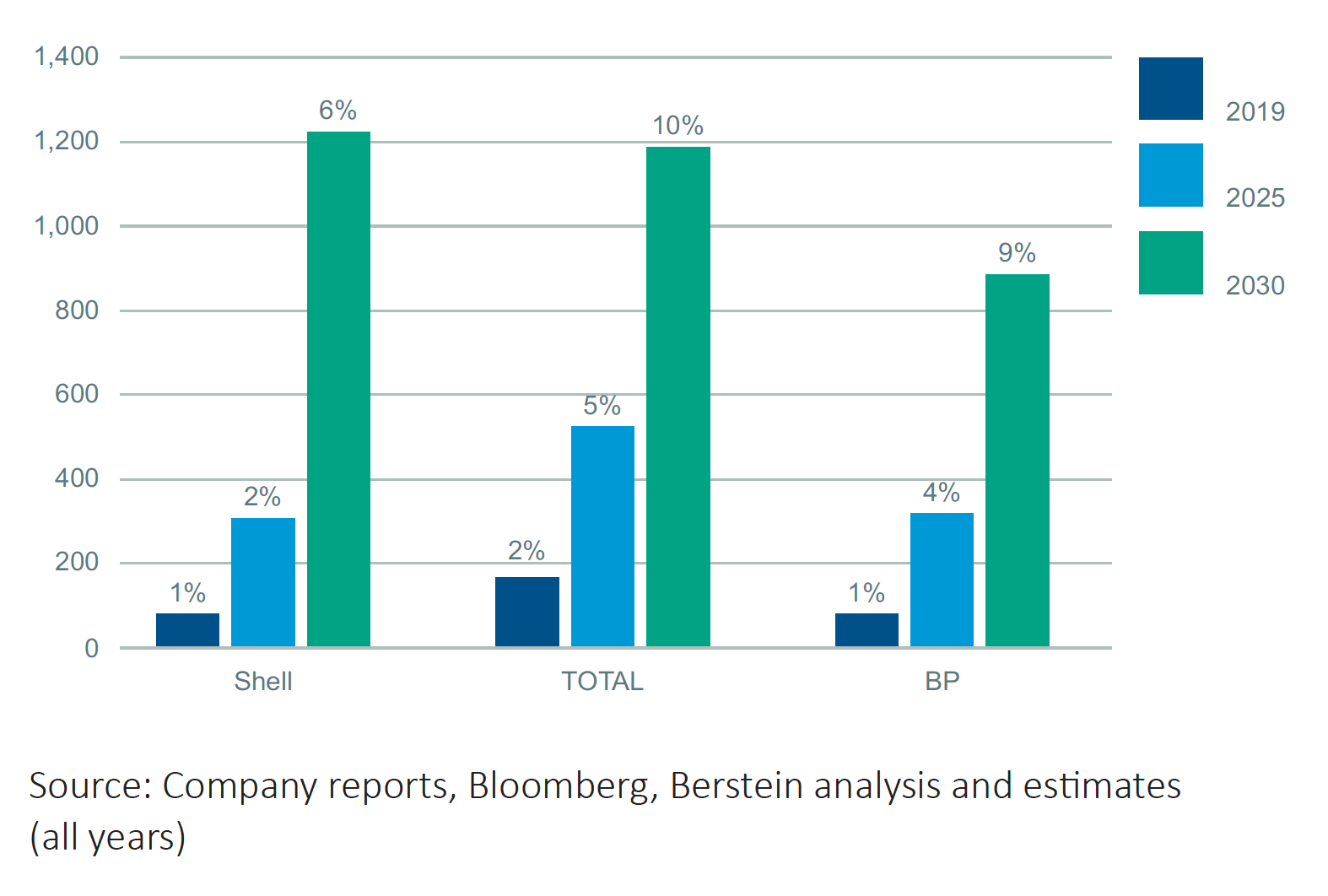

Bernstein estimates that by 2030 renewables will still represent only 10% or less of earnings for Shell, BP and Total.

Figure 2:

Earning Contribution From Low Carbon Business ($M)

Stranded assets

There is a serious risk that the oil majors will fall short of their transition targets – perhaps far short. The consequences for investors could be serious. Former Bank of England governor Mark Carney repeatedly warned about the perils of investors finding themselves in ‘stranded assets’. Now a UN special envoy for climate change and finance, he says up to 80% of coal assets and half of developed oil reserves could be left stranded. He has challenged asset managers to have a plan to mitigate that risk.

Professor Doyne Farmer, Director of the Complexity Economics programme at the Oxford Martin School at the University of Oxford, is currently producing a paper with the results of a model for the future of fossil fuel.

He says: “I think there’s going to be a major crash in the fossil fuel market, and it’s likely to happen within the next decade. Companies like BP get it and are taking steps to be players in the new world. Companies like Exxon Mobil don’t seem to be doing that. The foresighted fossil fuel companies are well positioned if they really aggressively transition, so that they can jump from one side to the other as the transformation happens. In our model we looked at the revenue stream that these companies have, and it gives them a competitive advantage. They have serious investment capital. If they can actually move their physical assets over from one technology to the other – and get the funding of that right – they potentially will be big winners here.”

Investment view

There is a scenario in which the oil majors do well. A rapid and synchronised post-Covid global recovery could see oil, gas and liquified natural gas prices quickly rise. Follow this with a successful transition to renewables and the picture looks good. Many analysts believe valuations on some European oil majors are attractive enough to warrant a contrarian bet on this scenario.

Our own view is that, while there are certainly legitimate arguments for investing in the oil majors, there are currently plenty of more appealing investment opportunities elsewhere. The precise date of peak oil is hard to guess, but it is undoubtedly closer than many analysts predicted even a few years ago. Like the huge seaborne tankers that oil companies depend on, turning these businesses around will not be an easy or quick process.

By Patrick Trueman, Portfolio Manager

Posted on 16 November 2020

1 IEA

2 www.iea.org/fuels-and-technologies/oil – from 2018 levels

3 www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/energy-outlook/bp-energy-outlook-2018.pdf

4 Financial Times: www.ft.com/content/21affff2-1e57-4000-a439-62cfef6344fb

5 www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/energy-outlook/bp-energy-outlook-2020-presentation-with-script.pdf

6 www.current-news.co.uk/news/renewables-near-50-of-generation-share-in-q2-as-records-continue-to-be-broken

7 www.statista.com/statistics/307194/top-oil-consuming-sectors-worldwide/

8 RenewableUK.com

9 Economist podcast, 20 September – 2020 www.economist.com/podcasts/2020/09/22/new-energy-order-how-clean-power-is-fuelling-geopolitical-changes

10 www.economist.com/business/2020/07/18/oil-giants-want-to-own-only-the-cheapest-cleanest-hydrocarbons

11 www.reuters.com/article/us-bp-writeoffs-idUSKBN23M0QA

12 www.reuters.com/article/us-bp-writeoffs-idUSKBN23M0QA

13 uk.reuters.com/article/uk-shell-outlook/shell-to-cut-asset-values-by-up-to-22-billion-after-coronavirus-hit-idUKKBN2410SJ

14 Data: 12 months to 28/10/20

15 www.economist.com/leaders/2020/09/17/is-it-the-end-of-the-oil-age

16 Looney speech: “Reimagining energy, reinventing BP”, 12 February 2020

17 BP August announcement.

18 BP wind investment details

19 ENI and Bernstein analysis

20 ENI and Bernstein analysis

…………………………………………………………………………………………………………

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.